Debt Resolution Outperforms Other Debt Help Options

Debt resolution, debt consolidation loans, bankruptcy, and traditional repayment plans share a common purpose: they are a pathway to getting out of debt. Although the end goal is the same, they employ very different strategies and can have significantly different impacts on your long-term financial health. The form of debt help you chose can impact your credit health, how much you spend on your debt and how long it takes you to repay it. Debt resolution is a straightforward option. With debt resolution, you’ll spend less money, get out of debt faster, and won’t have to deal with lawyers or judges.

Debt Help Options Overview

Debt resolution: Debt resolution means negotiating with your creditors to resolve your debt for an amount of money that is less than what you owe, including principal balance, fees, and interest owed. If you work with a debt resolution program, you’ll save money in a Dedicated Account while debt negotiation specialists work with your creditors on your behalf. When they reach a resolution agreement, the funds from your Dedicated Account will be used to pay the resolved amount.

Debt consolidation loan: This debt solution involves taking on a new loan to pay off multiple debts. This allows you to effectively combine multiple debt obligations into one, that you pay off with monthly payment. This helps streamline the repayment process for credit cards, loans, and other bills.

Bankruptcy: Bankruptcy is a legal proceeding in which all or a part of a debt is discharged by a judge. In order to file bankruptcy, the debtor decides which type they would like to file and petitions the court. In bankruptcy, the debtor’s assets will be evaluated and may be used to help repay the debt.

Making Minimum Payments: Minimum payments are a percentage of the debt that must be paid to the creditor every month in order for the debt to remain in good standing. The minimum payment is usually 1 to 3% of the balance on the debt. Interest that has accumulated on the debt, as well as any fees, are deducted from the minimum payment and the rest is used toward the principal balance. Making minimum payments is the slowest and most expensive method of repaying a debt.

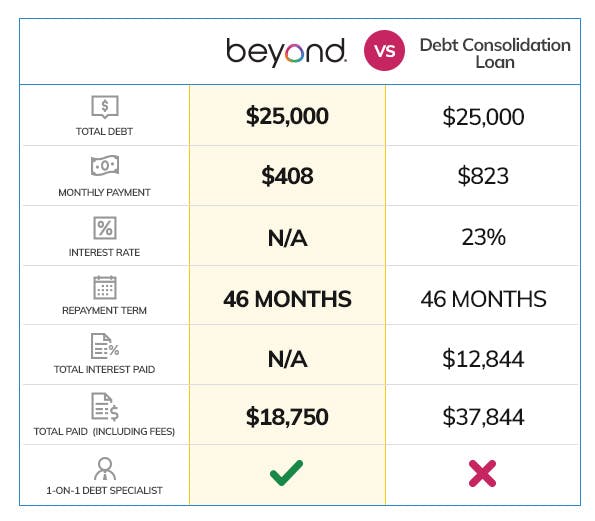

Debt Resolution vs. Debt Consolidation Loan

Both boast the ability to get you out of debt faster and for less money. The biggest difference between debt resolution and a debt consolidation loan is that consolidation requires you to take on new debt to pay off the old. Let’s take a look at how they work.

A debt consolidation loan can save you some money on your debt if you qualify for an interest rate lower than what you were paying before, but chances are good that you will need to pay as much, if not more, in monthly payments to pay down your debt. It could also take you a lot longer than if you chose debt resolution.

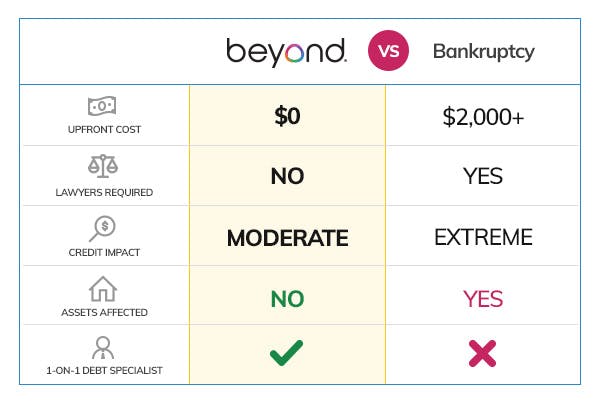

Debt Resolution vs. Bankruptcy

Debt resolution and certain types of bankruptcy involve closing your debts for less than what you owe. Depending on the type of bankruptcy you chose, you may be able to have all or a portion of what you owe discharged by the court. This is certainly helpful if you lack the resources to pay your debt, but taking legal action comes with its own set of consequences.

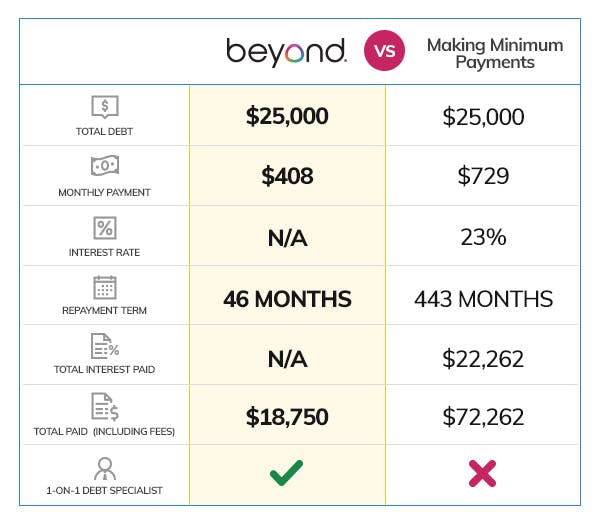

Debt Resolution vs. Making Minimum Payments

Minimum payments may seem reasonable at first, but when you crunch the numbers it’s easy to see how they actually trap you in a cycle of debt that can double or triple what you owe over time. As a general rule, if you can only afford to make the minimum payments on your debt, you can’t afford that debt and have a debt problem.

Debt Resolution can drastically reduce the amount of money you spend on your debt and speed up your repayment so that you’ll be debt-free faster. For example, if you owe $25,000 and make minimum payments it could take you more than 35 years and $47,000 to pay off your debts compared to a debt resolution program which could have you debt-free in 36 months.

The minimum payment example is based on a credit card for individuals with fair credit, having an interest rate of 23% (rounded up to the nearest percentage point) and assumes a payment of 3% of the balance. Please note that, assuming the principal balance does not increase due to additional charges, fees, and interest, the required minimum monthly payment will decrease over time as additional minimum monthly payments are made and reduce the total balance.

The Benefits of Debt Resolution

Debt resolution can save you a lot of money and time. Since you will only be paying a fraction of what you originally owed, you’ll be able to pay off the debt much faster once a resolution is reached. If you work with a debt resolution company, you also have the added benefits of working with debt negotiation specialists who are highly trained and experienced.

- Pay off debt faster

- Pay a fraction of what you owe

- Reduces your monthly payments during the program

Is Debt Resolution Worth It?

When compared to other forms of debt help (bankruptcy, debt consolidation loan, making minimum payments) debt resolution provides the most savings and clearest pathway out of debt. While debt resolution can lower your credit score, the impact can be overcome. Many clients feel that a moderate and repairable drop in credit score is worth the peace of mind they feel resolving their enrolled debts for good.

Debt resolution is the obvious choice for people who meet the following criteria:

- Ready to enroll $7,500 or more in unsecured, private debt

- Are able to make monthly payments based on the terms of your debt resolution program

Debt Resolution Is the Right Form of Debt Help for You

Being accepted into the Beyond Finance debt resolution program should boost your confidence that you are on your way to a future with less debt! That is because we only enroll clients who are a good fit for our program.

What You Can Do

While we work hard to get you a resolution offer for less than you owe, we know you’ll be able to handle a few key responsibilities that are essential to your success:

- Make regular monthly deposits to your Dedicated Account

- Approve offers when we send them to you

- Communicate with us whenever you have questions or concerns

Following these simple steps will help you see the program through and move toward your life after debt resolution.

Monthly Deposits Fuel Your Debt Resolution Journey

With other debt strategies, it’s easy to feel like the debt is in control—debt resolution puts you back in control of your debt. You can speed up the process at any time by increasing your monthly deposits or adding more money to your account.

Enroll Your Debt as Soon as Possible

Not enrolled yet? If your debt meets the requirements and you can commit to making monthly payments of $200 or more, speak to a Certified Debt Specialist as soon as possible. Our experts at Beyond Finance will walk you through the debt resolution process and help you pick a program that meets your needs. We are confident we can lower your monthly payments and help you pay off your debts for a fraction of what you owe.