How To Handle Debt Collectors

When you make changes to your payment habits, communication from debt collectors can be frequent and disruptive. Creditors and collection agencies can also be aggressive and intimidating. It’s important to know your rights and how to handle creditors and debt collectors when they contact you.

Reasons Creditors Will Contact You

Payment habits can change for different reasons. Common reasons a creditor or debt collector will reach out include:

- A problem with your account (fraudulent activity or other errors)

- Late payments

- Debt payment one month or more behind

- Debt has been transferred or sent to a collection agency

- Delayed payments when pursuing debt resolution with Beyond Finance

How Can Creditors Contact You About Debt

There are laws in place to protect consumers and govern how and when debt collectors can reach out to you about debt.

Creditors must abide by Federal Trade Commission rules outlined in the Fair Debt Collection Practices Act (FDCPA). These regulations prevent debt collectors from using abusive or unfair practices.

These rules apply per debt claim, which means folks with three or four outstanding debts can be contacted 7x in 7 days for each debt.

What To Do When Creditors Contact You

What Not To Do When Creditor Contacts You

- Make a payment if you have not verified the debt is yours

- Make a payment if you are already working with a debt resolution company like Beyond Finance

Debt Collectors Can Contact You on Social Media

In late 2021 the CFPB updated rules governing how creditors can contact consumers to collect debts. The new rule allows creditors to contact consumers about debt via emails, text messages, and social media platforms.

CFPB rules prohibit debt collectors from contacting you about debt on social media platforms if the message is viewable by the general public or your social media contacts.

Debt collectors can send you private messages over social media until you’ve asked that the debt collector not use that method to communicate with you. Also, suppose a debt collector sends you a private message via social media, like through Facebook or LinkedIn, asking to be added as one of your contacts. In that case, the collector has to disclose their identity as a debt collector.

While creditors are allowed to contact you on social media they must do so privately. Collectors can’t post on your page if it can be seen by your contacts or the public and rules and restrictions apply: they can only contact between 8 a.m. and 9 p.m., they must give you the option to opt-out and they can’t contact you more than 7x in 7 days.

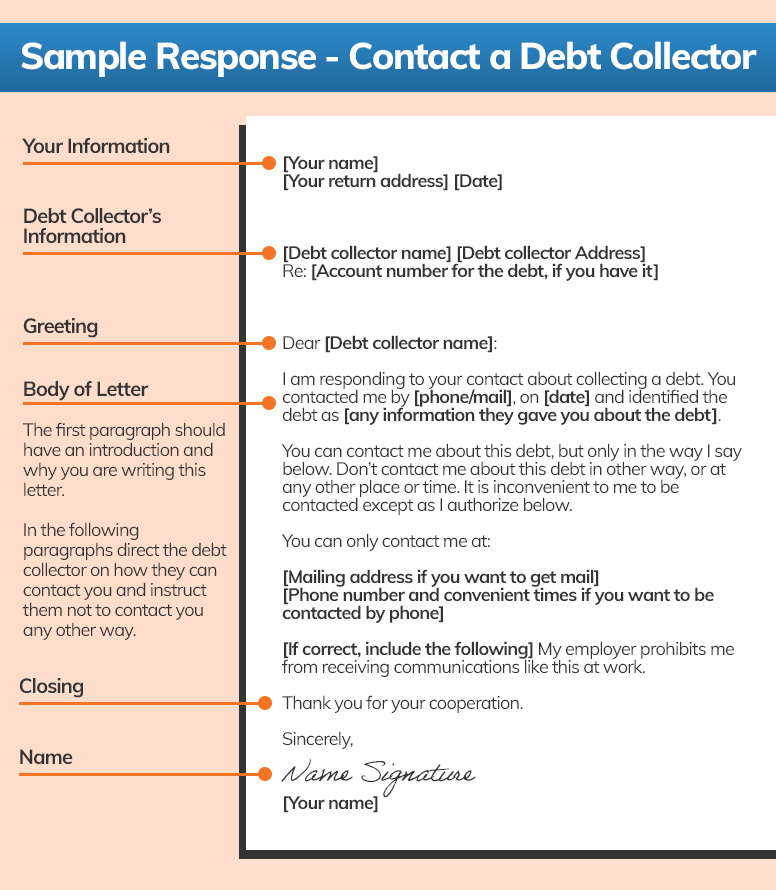

Sample Letters from the Consumer Financial Protection Bureau

The following sample letters from the CFPB will help you address problems that may come up with debt collectors like:

- I want to specify how the debt collector can contact me

- I need more information about this debt

- I want the debt collector to stop contacting me

- I want the debt collector to only contact me through my lawyer

- I do not owe this debt

How to Submit a Harassment Complaint

If you have made written requests and the collector is still harassing you, submit a complaint with the CFPB and Federal Trade Commission. You can also report them to your state’s attorney general.

Consumer Financial Protection Bureau

- File a complaint online

- Calling 855-411-2372,

Federal Trade Commission

- File a complaint online

- Call 877-382-4357